When Chinese student Yeva Zhang first started to dabble in make-up, she only had eyes for “Japanese and South Korean brands” but now the 18-year-old student has stocked her “vanity case with Chinese ones”.

Tempted to buy by social media advertisements and livestreamers, she says she can “hardly tell the difference” between cheaper local brands and some of the biggest names in global beauty.

Local companies are nipping at the heels of global names such as L’Oréal, Estée Lauder and Shiseido in China, the world’s second-biggest beauty market by sales. Their savvy use of social media and concentration on less affluent cities overlooked by foreign firms has helped them gain ground.

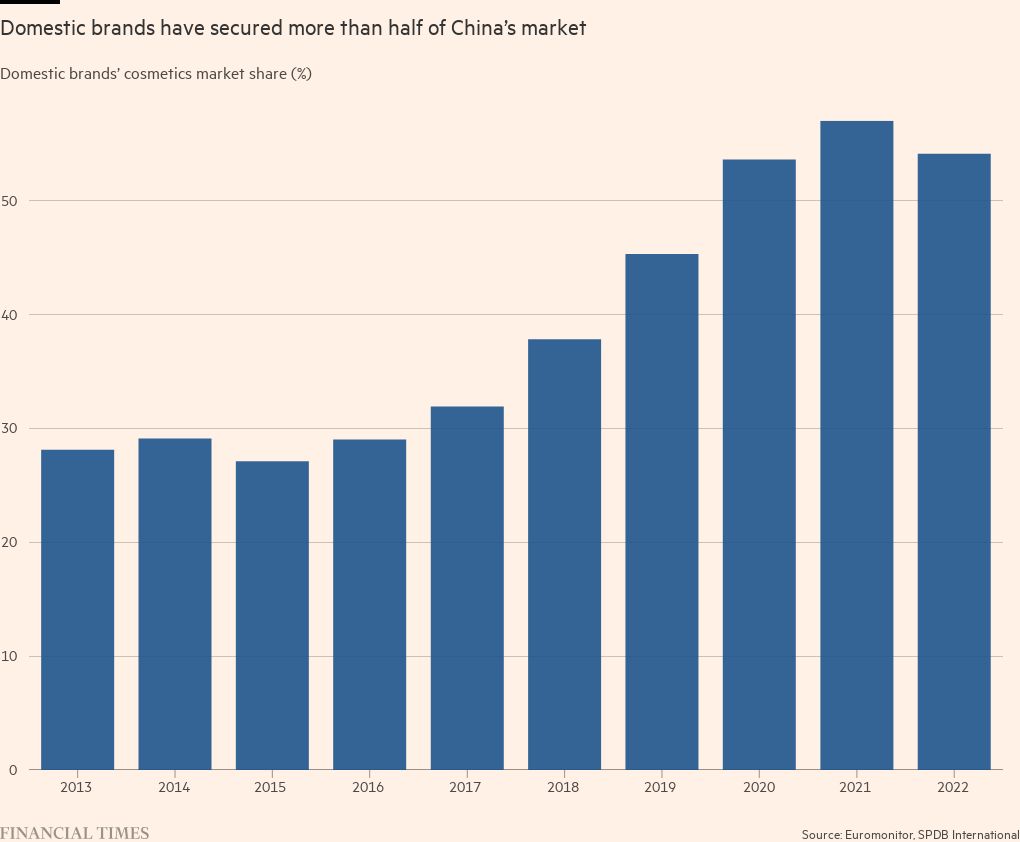

Domestic labels’ share of 40 top beauty brands’ online sales in China rose to 47.9 per cent in the first 10 months of 2023 from 43.6 per cent a year earlier, according to data from Euromonitor. It forecasts that China’s colour cosmetics market, which includes products such as foundations, lipsticks and nail polishes, will hit Rmb111.3bn ($15.6bn) in 2028, up from Rmb71.6bn in 2022.

“It is the best of times for Chinese brands, as consumers’ level of openness for them has never been higher,” said Miro Li, founder of Shenzhen-based marketing consultancy Double V Consulting.

TikTok’s Chinese app “Douyin has successfully approached a wider range of consumers, particularly younger people in lower-tier cities, who are out of reach of traditional ecommerce sites such as Tmall”, said Stefan Huang, head of strategy at Shanghai-based Joy Group, which is backed by General Atlantic and owns two local cosmetics brands — Judydoll and Joocyee.

“A number of foreign companies didn’t catch up with the trend, but Chinese brands did,” he said. L’Oréal, for example, only started ramping up its marketing on Douyin in 2023.

Sales on social media are set to become even more important, with Goldman Sachs calculating that a combined 37.5 per cent of China’s total ecommerce cosmetics transactions will take place on Douyin and its rival Kuaishou in 2025, up from 25 per cent in 2021.

“Many foreign brands, including [those in] cosmetics, took a hit during the zero-Covid years as many decision makers based outside of China became increasingly disconnected to a fast-changing China,” said Mark Tanner, managing director of Shanghai-based branding agency China Skinny.

The other advantage local companies have on foreign brands is domestic marketing teams and close access to factories, said Huang.

“If I spot a lipstick shade that is losing momentum or a new trend that is about to take off, I can get to the factory within two hours and adjust the production within a month,” said Huang. “It normally takes a foreign brand four to six months to respond [to consumer preferences change].”

There is still room for foreign brands to grow. Shiseido, which made 26.4 per cent of its sales in China in the first half of 2023, said in a written reply that it would increase its investments in both “promotional activities” and “brand value building” in China. Estée Lauder and L’Oréal did not respond to a request for comment.

L’Oréal’s sales in North Asia, which is dominated by China, totalled €11.3bn in 2022, about a third of its sales that year, and up 6.6 per cent year-on-year despite harsh zero Covid lockdowns denting sales in the last quarter. Their premium luxury division in China in particular has been steadily gaining market share. Though sales in their most recent quarter in North Asia declined 4.8 per cent compared with the previous year due to changes to China’s rules about offshore daigou shopping, in the mainland they grew 7.7 per cent over the period.

“We’ve gained very strong market share for luxury in China. The anecdote is that right now we have a market share for L’Oréal luxury in mainland China, which is above 30 per cent which is equal to the sum of its two next contenders — which is not bad,” L’Oréal chief executive Nicolas Hieronimus told the Financial Times in an interview last year.

Even as Chinese cosmetic companies gain ground, they risk becoming trapped in a “vicious cycle” of being a cheap substitute for foreign brands, said Li from Double V Consulting.

Florasis, a Hangzhou-based cosmetics start-up and the country’s largest local beauty brand with a 6.8 per cent market share, has made some inroads into the premium market. It has been helped in part by influencers such as Li Jiaqi, known as the “lipstick king”. But it suffered a backlash last year after livestreamer Li criticised a viewer for not earning enough to buy Florasis’s eyebrow pencil worth Rmb79. He later apologised.

The company says its prices are justified by its more than Rmb10bn investment into R&D infrastructure and high-cost packaging. “There’s no copycat of us in the market because it’s too expensive to make [our products],” said Gabby Chen, president of global expansion at Florasis.

Florasis hopes to replicate its formula of vast social media presence and traditional Chinese motifs in overseas markets including the US, Japan and south-east Asia. Joy Group has also set up operations in countries including Japan, Malaysia and Canada.

“They have been raised in China’s hyper-competitive marketplace” so they may have an advantage in a “slower moving marketplace abroad”, said Tanner from China Skinny. “We saw this with [fast fashion brand] Shein, which didn’t do anything special by Chinese standards . . . There is no reason Chinese beauty brands couldn’t do this too.”

Additional reporting by Adrienne Klasa in Paris